Key takeaways

- You may be eligible to apply for an additional loan through Upstart, but approval depends on your current financial profile.

- Borrowers may apply for additional loans within the same product category or across different loan types.

- Checking your rate can help determine current eligibility without affecting your credit score.

If you’ve already taken out a personal loan through Upstart, you know how simple and seamless the process is. The next time something unexpectedly comes up, and you need to borrow money, you might wonder whether you can take out a second personal loan, even if you’re still working on paying off your first loan.

The answer is yes—if you meet specific qualifications. We’ll walk you through how to figure out if you’re eligible to get a second personal loan through Upstart and, if you are, how the process works.

Am I eligible to get a second personal loan through Upstart?

Eligibility for an additional loan through Upstart is based on a comprehensive review of your financial information at the time you apply. While specific criteria may evolve over time, your application will be reviewed based on key factors, such as:

- Meeting general credit and financial criteria

- Verifying income and ability to repay

- Residing in an eligible state

- Complying with any waiting periods between loans

Meeting these requirements does not guarantee approval, but it allows you to proceed with an application for further review.

Do you need to wait before applying for a second loan through Upstart?

Yes, there may be timing considerations to apply for a second loan through Upstart, depending on your loan history and current product guidelines. We work with borrowers who need to take out a second personal loan, within limits. And we understand if you need to borrow more money—but to ensure you’re not overburdened, we’ve set up key criteria if you’re still paying off your first loan through Upstart or have already paid off your first Upstart-powered loan.

However, remember that eligibility is not determined by a single factor such as a fixed waiting period. Instead, approval depends on your overall financial profile and product-specific criteria at the time of application.

Can you have more than one active loan through Upstart at the same time?

Its possible that borrowers may qualify for more than one active loan through Upstart. This could involve:

- An additional personal loan

- A new type of loan

If you currently have a personal loan, you may also be eligible to apply for other type of loan through Upstart, such as:

- Short-term Relief — designed for smaller borrowing needs

- Auto secured personal loan — allow borrowers to use their vehicle as collateral to obtain financing(If Upstart determines that an auto secured loan is an available option for your personal loan, an auto secured offer will be presented).

- Home equity lines of credit (HELOCs) — secured by available home equity

Each product has its own underwriting process and requirements. Approval for one loan type does not automatically qualify you for another.

How to apply for a second loan through Upstart?

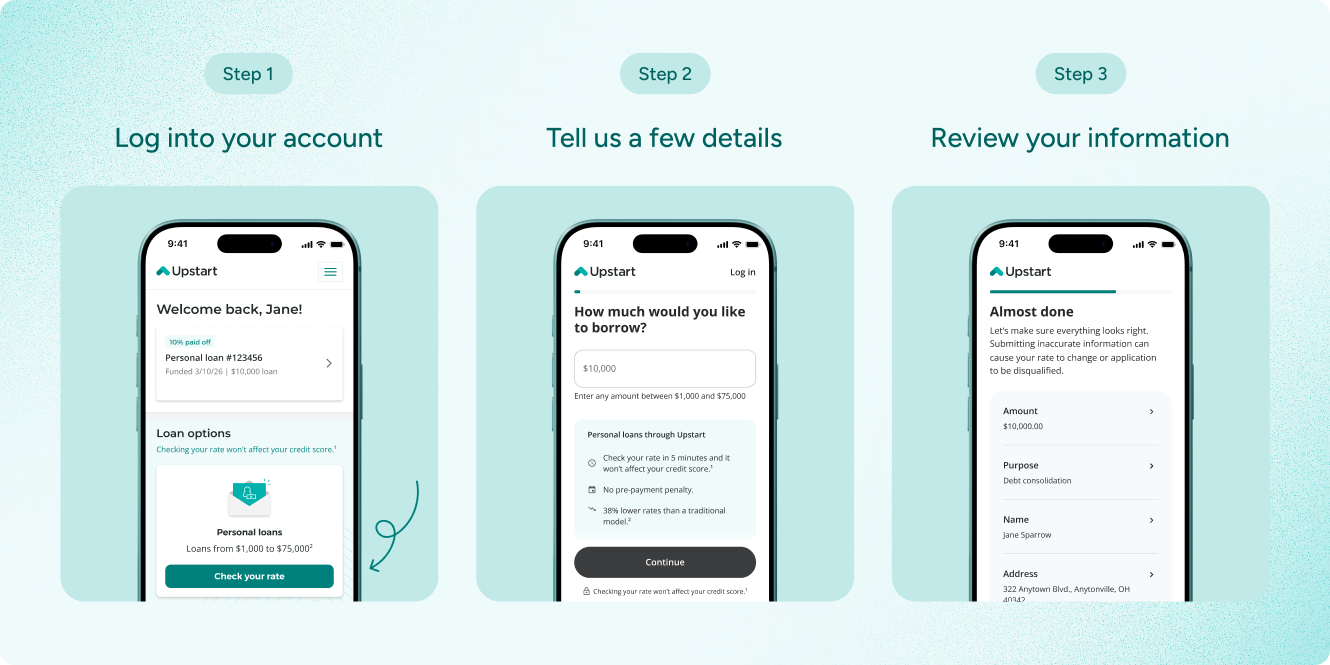

If you’ve taken out a loan through Upstart before, you may know the process to apply for a second loan through Upstart is designed to be straightforward. If you’re eligible to apply for another loan, you can start the process directly from your Upstart account:

- Log into your account and look for available loan options – Navigate to My Account, where you will see your existing loan details. Look for available loan options – If you’re eligible to apply, you’ll see available loan options displayed as separate cards below your active loan.

- Tell us a few details

- Review your information

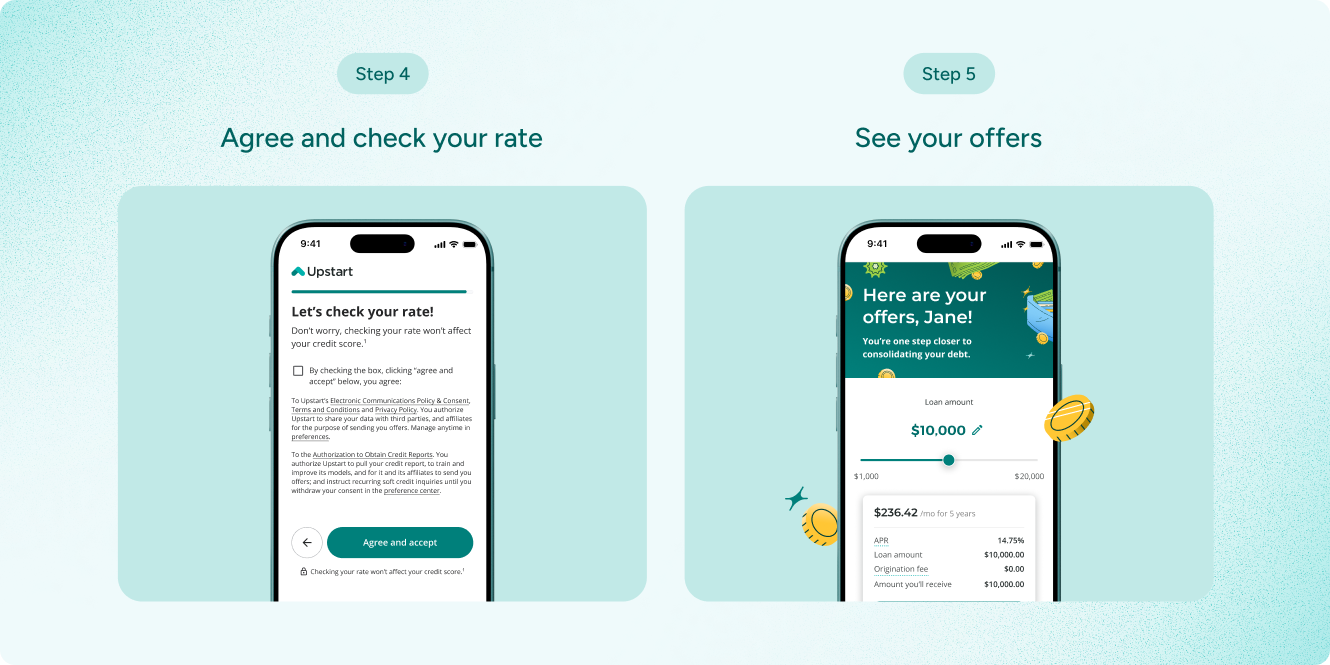

- Agree and check your rate

- See your offers. If you decide to move forward, you can complete the application from there.

Note: Seeing a loan option in your account does not guarantee approval. Eligibility is confirmed only after you check your rate and complete the application process. If you don’t see an option to check available loans, you may not currently meet the eligibility requirements.

What happens to your credit when you apply again?

Checking your rate typically involves a soft credit inquiry, which does not affect your credit score. If you decide to submit a full application, a hard credit inquiry may occur, which can temporarily affect your credit score.

Pros and cons of taking out a second loan through Upstart

Taking out an additional loan can be helpful in some situations, but it also increases your financial commitments. Before applying, it’s important to weigh both the potential benefits and the trade-offs.

Potential benefits

- You can access additional funds when needed: Taking out a second loan can help you unlock new possibilities, such as moving to a new part of the country, getting the medical care you need, or consolidating high-interest credit card debt to make it easier and simpler to pay off.

- You may qualify for a different rate based on your current credit profile: If you didn’t miss any payments on your previous loan on Upstart, your credit score might have gone up since you last applied. That means you may be able to get a better rate, too.

- You’re already familiar with how Upstart works: Since you’ve already taken out a loan through Upstart before, you’re already familiar with how things work. You’ll know what documents you need, what to expect, and how to manage your loan because you’ve done it before.

- Flexibility across loan products. Depending on your situation, you may be eligible to apply within the same loan category or across different loan types.

Important considerations

- Increased monthly obligations

Taking on another loan means adding a new payment to your budget, which can affect overall financial flexibility. Remember to save up for emergencies and other financial goals, too.

- Impact on your credit profile

Applying for and managing additional debt may influence your credit score, especially if total balances increase.

- Eligibility is not guaranteed

- Approval for another loan depends on your current financial profile and underwriting review at the time of application.

Before applying for an additional loan, you may want to consider:

- Your total monthly debt obligations

- Your repayment performance on current loans

- Whether your income supports additional payments

- The purpose of the new loan

Understanding how an additional loan fits into your broader financial plan can help you make an informed decision.

Check your rate on a second loan

If you need to borrow money, consider checking your rate on a new loan through Upstart. You might find that you may qualify for an even better rate this time, and that can make paying off your new loan even easier than before.

FAQs about getting another loan

Can I apply for another loan before paying off my current one?

In some cases, yes. Eligibility depends on your repayment history, financial profile, and product guidelines at the time of application.

Is there a required waiting period?

Yes, there may be a waiting period before applying for another loan. Timing considerations can change over time, and eligibility is based on multiple underwriting factors at the time of application. To learn more, you can check your rate for another loan through Upstart.

Can I apply for a different loan product if I already have one?

Possibly. Each product has its own eligibility requirements, and approval is evaluated separately.

Does applying again affect my credit score?

Checking your rate generally uses a soft credit inquiry1. A hard inquiry may occur if you submit a full application.

Won't affect your credit score¹

Won't affect your credit score¹