Debt Consolidation Loans

Lower your rate. Simplify your debt.

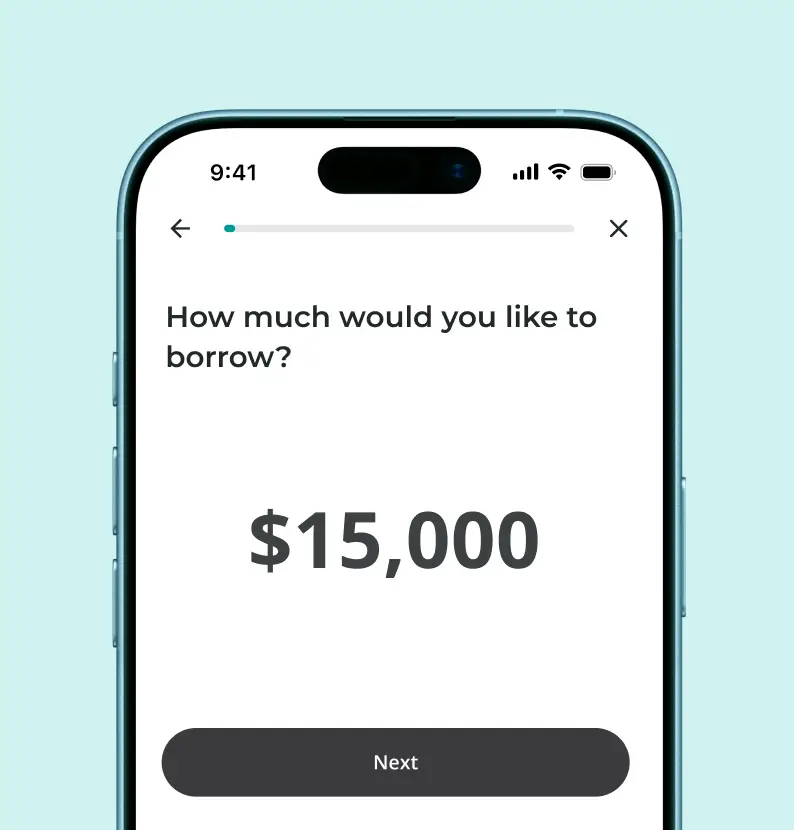

- Check your rate in 5 minutes

- Cash sent in as fast as 24 hours³

- Consolidate your bills into 1 fixed monthly payment

BENEFITS of Upstart Loans

Why consolidate debt with Upstart?

Save on interest with a lower APR⁸

You could take control of high-interest debt or multiple bills by consolidating your balances into one lower-interest loan—we find 33% lower rates than traditional models.¹¹

Get clear terms that help you feel in control

There’s no surprises—see your rate, monthly payment and total costs before you commit. And with no prepayment penalties, you can pay your loan off on your terms.

Apply quickly and get cash fast

With our 100% online process, you can check your rate in minutes. If approved, you could get cash sent to you in as fast as 24 hours.³

You could take control of high-interest debt or multiple bills by consolidating your balances into one lower-interest loan—we find 33% lower rates than traditional models.¹¹

Debt Consolidation vs Credit cards

How much could you save by consolidating your debt?

| Personal loan | Credit card balances | |

|---|---|---|

| APR | 18% | 24% |

| Monthly payment | ~$381 | ~$432 |

| Payments per month | One | Multiple |

| Estimated interest paid | ~$7,860 | ~$10,891 |

| Estimated interest saved | ~$3,000 | $0 |

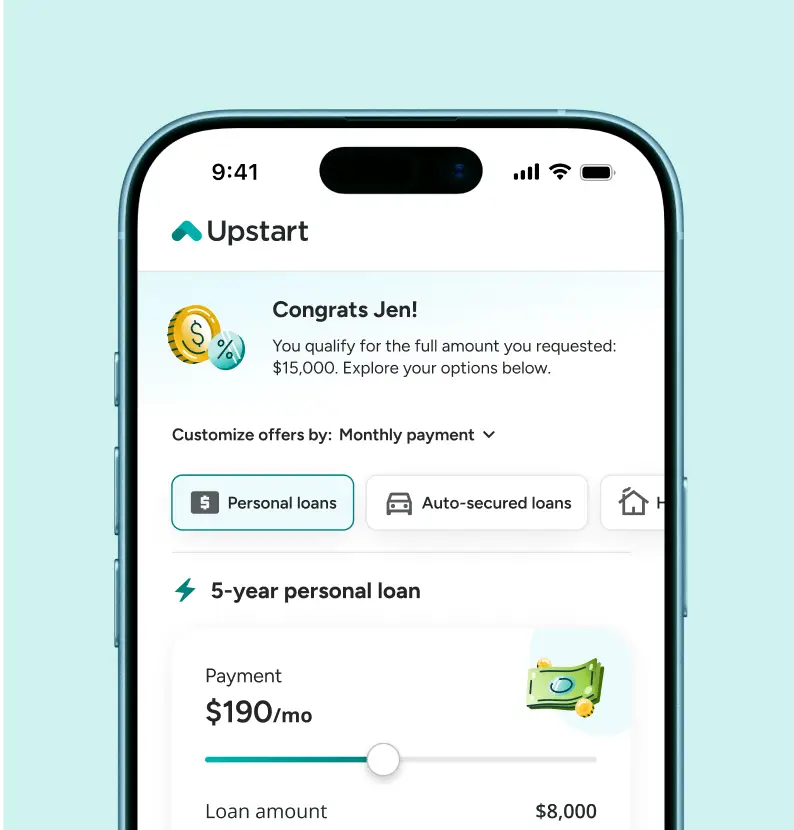

Find out if you’re approved, instantly⁶

Apply right from your phone—no paperwork required.

Easy online loan application

How to apply for a loan through Upstart

Check your rate

It takes less than 5 minutes to check your rate—and it won’t affect your credit score.⁵

See your options

Find out if you're approved, instantly with no paperwork required.⁶

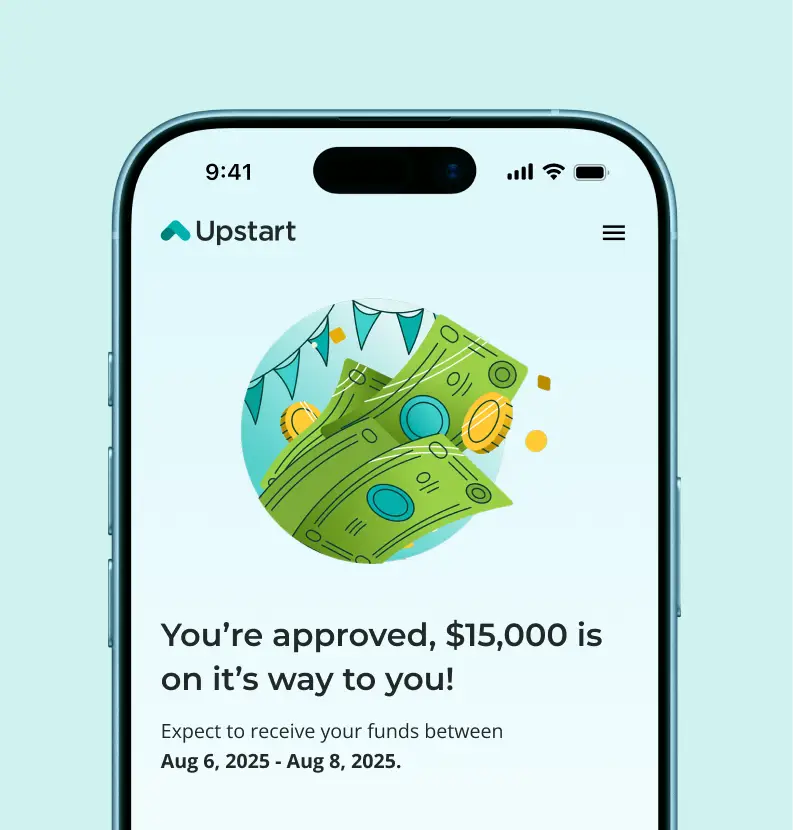

Get your funds

If approved, you could get funds sent in 24 hours.³

We’ve helped over 2.7 million customers consolidate their debt¹³

Get the money you need when it matters most—apply in minutes.

UPSTART Reviews

Real reviews from real customers

Upstart is rated 4.9 out of 5 on Trustpilot, based on over 50,000 Upstart reviews from verified borrowers¹.

Customer photos may be fictitious.

Got a debt consolidation loan quickly and easily online with almost instant approval.

How Marcus Reunited His Family with a Personal Loan

Read the full storyI was looking to consolidate some debt. I had used Upstart in the past and had a good experience, so I decided to go through the process again. It was quick, easy, and secure.

How Holly Paid Off $9.9k in Credit Card Debt

Read the full storyIt's exciting to cut my debt APR almost in half by using this to pay down my credit cards.

How Ashley Overcame Family Debt and Improved Her Credit

Read the full storyCustomer photos may be fictitious.

Frequently asked questions